2022 Outlook

2022 has dawned with heightened volatility and concerns that a prolonged market downturn is imminent. We view 2022 as a bit of a mixed bag in terms of market risk and opportunity and perhaps have a more nuanced view than many. For this month’s Insights, I thought it would be constructive to spend some time on key themes that we feel will drive market performance and our views on the same. In 2022, we’re focused on the following:

- Inflation

- Geopolitical Risk

- COVID

- Legislative Risk

- Corporate Earnings

After touching on these topics, we’ll outline our playbook for both the opportunities and challenges we see in the coming year.

Inflation

Rather than a discussion of the ins and outs of inflation as this topic has been covered ad nauseum in popular press, I’d like to focus on the key risks that inflation presents in 2022:

Risk #1: The Federal Reserve doesn’t do enough to rein in inflation

Risk #2: In its attempts to rein in inflation, the Federal Reserve severely harms economic growth

Risk #3: In spite of #1 or #2, embedded inflation expectations lead to prolonged price instability

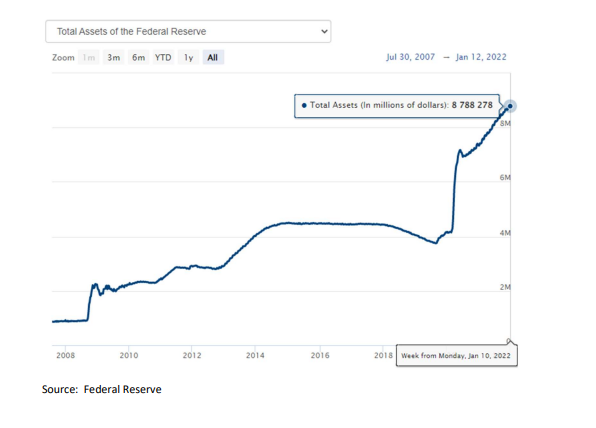

Let’s begin with Risk #1. This is a very real concern as for much of 2021, the Federal Reserve would speak about “transitory” inflation and seemed to isolate much of the inflation to supply chain issues coincident to COVID. This runs counter to the idea presented by the famous economist Milton Friedman who stated, “Inflation is always and everywhere a monetary phenomenon in the sense that it is and can be produced only by a more rapid increase in the quantity of money than in output.” Our thesis is that while some of the inflation we’re seeing has been driven by COVID issues, much of it stems from the rapid expansion of the money supply. Easy money policies and the expansion of the Fed’s balance sheet have provided fertile ground for inflation to flourish:

As we can see above, the Federal Reserve has added over 4 trillion worth of assets to their balance sheet since the start of the pandemic. Our concern is that the Federal Reserve could be too cavalier about inflation and as a result, inflation expectations become more entrenched and harder to cycle out of. The inflation of the 1980s took strong medicine (prolonged high interest rates and consequently slower economic growth) and it remains to be seen if the Fed has the will to apply sufficiently strong medicine to adequately tamp down inflation.

Risk number two in our view is a less likely outcome-this current composition of the Fed has been decidedly dovish, but nonetheless warrants mention. The risk here is that the Fed overshoots on the speed and amount of rate increases and pushes the economy towards recession. Recession leads to lower profits and consequently, lower stock market values Risk number three is that in spite of the Fed’s efforts, inflation is entrenched in the economy and we either live with a prolonged period of high inflation or to tamp down inflation, a prolonged period of high interest rates and austerity. Either is a poor outcome, but in our view, we’ve yet to cross the threshold where it’s too late to shift price expectations. The Fed, however, does have a difficult balancing act where they need to balance the need to be sufficiently tough to beat back inflation, but not so tough that they harm economic growth.

A possible outcome for 2022 is a “sacrificial” year in terms of monetary policy. That is to say that the Fed sacrifices current growth in order to place the economy on firmer footing for the future via tighter monetary policy. This would mean that the Fed does move forward with anticipated rate increases, does begin to unwind their balance sheet and we see increases in mortgage rates, bond yields and various other rates. This scenario will harm growth stocks (higher interest rates reduce the current value of future earnings; we’ve started to already see this dynamic with recent Nasdaq selloffs) and bonds (bond prices move inversely to rates).

Geopolitical Risk

Geopolitical risks are inherently unpredictable-both in terms of the events and subsequent market reaction. Planning and preparation for these events is difficult as under-concern can lead to outsize exposure, while myopia and outsized focus on these can lead to significant missed opportunities. In our playbook section we’ll share some thoughts on how to best prepare for these types of events, but here we outline those that we worry the most about:

1. Russia/Ukraine. We view the situation here as a high likelihood/moderate impact (in terms of the stock market reaction) event. While a full-scale invasion may or may not occur, some level of engagement appears likely. It may come in the form of partially seizing segments of eastern Ukraine or further non-conventional activities (cyberattacks, ununiformed hostiles, etc.). A broad invasion would likely elicit a sharp, knee-jerk market reaction, but one that would be short-lived provided that broader escalation doesn’t occur.

2. Iranian Nuclear Program. Here all indications are that Iran is nearing minimum thresholds for nuclear weapon development and Iran does have a stated desire to destroy Israel. Israeli policy is that under no circumstance, can Iran be permitted to have a nuclear weapon. Over the years, Israel has taken repeated action to stymie and set back this program and pre-emptive military action seems likely should Iran make much more progress. This too is a higher likelihood/moderate impact event (with the same caveat that broader escalation doesn’t occur). This does not appear to be as imminent as the Russia/Ukraine situation, but barring a diplomatic solution, some action of note appears likely over the next several years

3. China/Taiwan. The situation here is lower likelihood, but far higher potential impact. Action here would be potentially expansive depending on the global response. At a minimum, we would likely see an immediate market shock and potential recession as global supply chains and the global order around trade and finance could be upended. Pundits have covered China’s capability to launch an invasion and likelihood that they’ll do so, so we won’t do so here, but we mention this risk as the potential shock to markets and the global economy is severe

COVID

We won’t spend too much time here other than to state our thesis around the pandemic’s ongoing impact to the economy and capital markets:

1. While COVID will continue to dominate headlines, the market will continue to be increasingly quick to shake off negative COVID news

2. Barring a more virulent strain, 2022 will see significant progress toward endemic status and a gradual easing of COVID-era restrictions

Legislative Risk

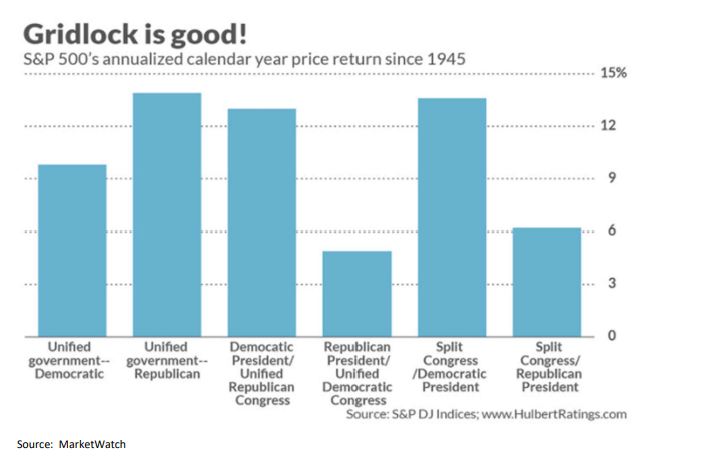

Our thesis for 2022 is that the potential for significant, market moving legislation (i.e. corporate tax increases, capital gains changes, “Green New Deal” provisions, etc.) has become increasing unlikely. The tail end of 2021 was marked by legislative impasse and it doesn’t appear likely that 2022 will be very different. Key swing senators appear to be dug in on disputed positions and barring significant changes of heart, large changes seem unlikely. Additionally, both history and recent data suggest a strong likelihood that the House of Representatives changes hands in the mid-term elections. Between this year’s likely stalemate and a potential for a change in the House, legislative gridlock seems likely for potentially up to three years.

Markets historically like gridlock:

Corporate Earnings

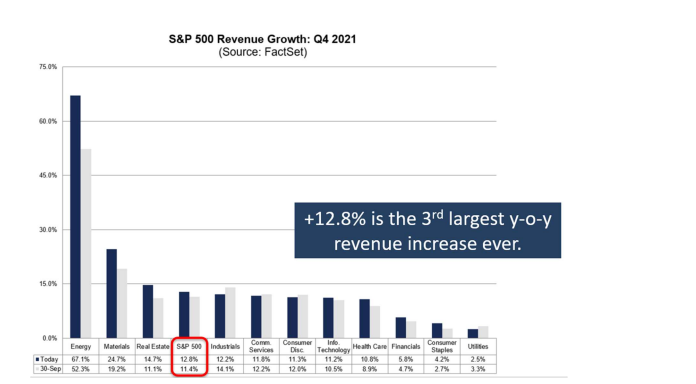

Earnings consistently drive stock prices in the long run and lost on many people is how remarkably strong earnings have been. Last year, we saw near records of revenue growth, and profit margins have been outstanding

The earnings outlook for 2022 is a little more uncertain than last year and we’ve seen some worrisome earnings on the tech side (i.e, Meta/Facebook) and concerning potential trends (underwhelming Netflix subscriber growth). On the other hand, Alphabet (Google) recently reported stellar earnings. The economic response to higher interest rates will be a key driver of how earnings play out over the course of this year and we’ll be watching this closely.

Playbook

We have some thoughts on how to take advantage of 2022’s opportunities and to manage risk. Please keep in mind that these are general observations and implementation of any of these strategies should first be reviewed with relevant professionals (Financial Advisors, CPAs, Attorneys). Below are some items to consider in no particular order:

1. Diversification remains key (when in doubt go over rather than under)

The January market pullback has underscored the need for an appropriately diversified portfolio. We would characterize 2022 as a low-conviction year (meaning our degree of confidence around potential market outcomes is lower relative to other years). In our view, as confidence in outcomes diminishes, the degree of diversification should increase. Consider insurance products, tactical strategies (those that preemptively try to avoid steep losses), and out of favor asset classes (i.e. international holdings) to provide diversification you may not currently have. Additionally, many investors have been light in value positions over the past several years and these can be an important part of a well-constructed portfolio.

2. Know the risks of bonds

We have had a multi-decade bond bull market that appears to be winding down. The trend for decades has been an overall trend down in interest rates and this has provided a strong tailwind for bonds to appreciate in value (bond prices

move inversely to rates; when rates go down, all things being equal, bond values will go up). The interest rate/price dynamic is exacerbated by the maturity of the bond. Long-dated bonds are more exposed to the risk of rising rates than shorter dated bonds. We therefore like the general idea of shorter-dated bonds in one’s portfolio. In the coming years, we view a bond market that will face continual headwinds with persistent structural forces that push rates upward. We

also view, however, that bonds will continue to provide balance and a diversification effect during periods of market downturn. Bonds still play a role in a well-constructed portfolio, but the credit quality of the bonds, the maturity of the bonds, and the overall weighting of the bonds should be thoughtfully considered.

3. Consider adding insurance to your portfolio

This point is mentioned in #1, but also warrants a second mention here. Many insurance products provide contractual principal guarantees that market-based investments cannot provide. Additionally, insurance products can provide some

tax advantages that investments may not be able to provide. There is an inherent tradeoff with insurance products often having lower internal rates of return and potential limited liquidity, but for many, having a portion of a portfolio in guaranteed insurance buckets can make sense. During downturns, these products can provide significant ballast to one’s overall portfolio.

4. Don’t be afraid of international holdings

All things being equal, we view US markets as having more inherent stability and upside relative to international markets, but international holding should play a role in most portfolios. Over the past decade, international holdings have vastly

underperformed US holdings and as we eventually come out of COVID-19, international holdings stand to disproportionately gain. For many of our clients at or near retirement, we’ve been targeting up to 10% of portfolios in international holdings.

5. Dry powder for downturns and consider dollar cost averaging in

Many investors have the wrong approach when adding new money into investments. Many will enthusiastically add excess cash when markets are significantly up, yet are skittish about adding cash when markets are down. While one never wants to catch a falling knife (buying too prematurely into a rapidly declining market), downturns often present great opportunities to buy assets that were previously overpriced. If one is concerned that a decline may continue but would still like to invest excess cash, consider dollar cost averaging (adding money in smaller increments over time rather than a lump sum all at once) into your desired investments. For example, if markets were declining and one had $500,000 to invest, one might consider adding $100,000 to investments each week over a five-week period rather than the full $500,000 all at once.

6. Consider roth conversions and tax loss harvesting on big dips

Large dips (15-20%+) can provide some good opportunities for roth conversions. Let’s consider a textbook example:

- Individual wants to convert $100,000 in investments in their traditional IRA to their roth IRA

- Because of market declines, the value of this $100,000 falls to $80,000

- While the portfolio is at $80,000, client convert the traditional IRA investments to a roth IRA

- Client pays taxes on the $80,000 instead of the $100,000

- Subsequent market rebound brings balance in roth IRA from $80,000 to $100,000

The market doesn’t always fall in line with this example, but if one is on the margin for converting based on projected tax rates and withdrawal timelines, a market dip may tip the scales in favor of converting. Additionally, market dips provide opportunities for tax-loss harvesting in non-qualified accounts. One must comply with IRS wash sale rules, but dips provide an opportunity to bank losses against future gains.

7. In light of the stellar performance over the past several years, consider taking profits and scaling back risk

We’ve experienced tremendous markets over the past several years and notwithstanding the recent pullback, many portfolios are up significantly overall going back many years. If you have a desire to pivot some of the gains into more conservative investments or if you find your risk appetite may have materially changed, it may make sense to do some profit taking. Profit taking simply means pivoting a portion of the money out of your appreciated positions into more

conservative positions or in extreme cases, cash. Care should be taken that any adjustments here are measured and correctly motivated (not a visceral reaction to a pullback).

We wish all of you and your families the very best in 2022 and are ever appreciative of the trust you place in us as your advisors.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

Diversification, asset allocation and rebalancing strategies do not ensure a profit and do not protect against losses in declining markets. Rebalancing may cause investors to incur transaction costs and, when rebalancing a non-retirement account, taxable events may be created that may affect your tax liability.

Investing involves risk, including loss of principal. Supporting documentation for any claims or statistical information is available upon request.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed. Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve. Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Alliance Wealth Advisors, LLC, is registered as an investment advisor with the SEC and only transacts business in states where it is properly registered, or is excluded or exempted from registration requirements. SEC registration does not constitute an endorsement of the firm by the Commission nor does it indicate that the advisor has attained a particular level of skill or ability a SEC Registered Investment Advisor – 150 N. Main St. #202 Bountiful, UT 84010